For most leadership teams, annual planning begins later than it should. The best planning processes take several months, from thinking through core assumptions and strategic bets to setting territories, compensation, and quotas and rolling them out to the team. But it’s challenging to dedicate attention to next year when you are trying to execute on the current year plan, and even more so if the current-year plan has gone sideways.

Our research and conversations with CEOs, CFOs, and commercial leadership teams indicate that planning for 2026 is going to be more complicated than usual, and also much more critical to get right. As a result, it’s essential that leadership teams avoid sacrificing strong performance in the coming year by delaying or giving only surface-level attention to forward planning. In this article we’ll dig into five big realities driving this need for deepened attention to planning for 2026.

Market Uncertainty is Higher Than Ever

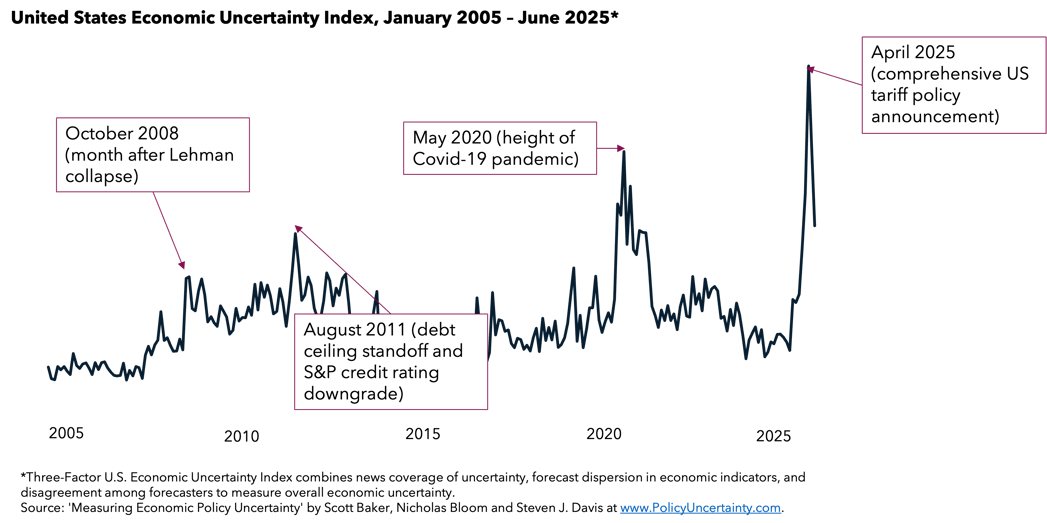

The first half of 2025 introduced significant market uncertainty. In Q2 in particular leadership teams operated amid the highest levels of policy uncertainty measured in decades. Looking, for example, at the U.S. Economic Uncertainty Index, we found that discussions of uncertainty were already in March 2025 exceeding the previous peak of May 2020, when the world was grappling with the implications of COVID-19 related lockdowns.

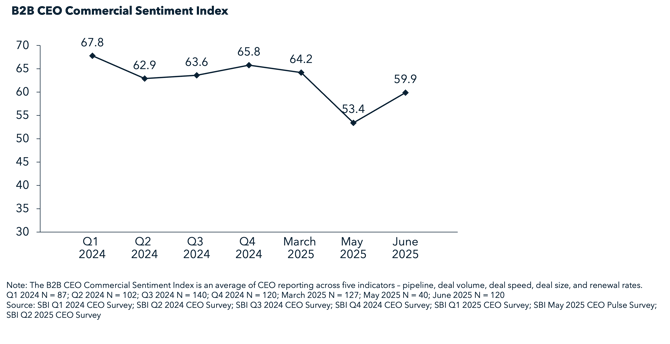

And this uncertainty trickled directly into business decision-making, slowing deal cycle times substantially, and forcing many to second-guess their growth plans. Our tracking of five indicators of commercial sentiment — pipeline quality, deal volume, deal size, deal cycle times, and renewals — found that while the year began somewhat sluggishly for many organizations, overall sentiment was generally positive. This took a deep dive in May to the lowest levels we have seen since we began tracking. While recovering somewhat in June, signs of volatility and tempered buying remain dominant.

Market uncertainty is likely to continue as companies adjust to both a new policy environment and business transformation brought on by artificial intelligence. This will make it harder to establish and agree on the core assumptions underlying the growth plan. Leadership teams will need more lead time and a much more robust fact base than in years past to get it right.

Companies Are Getting Low Return on Commercial Spend

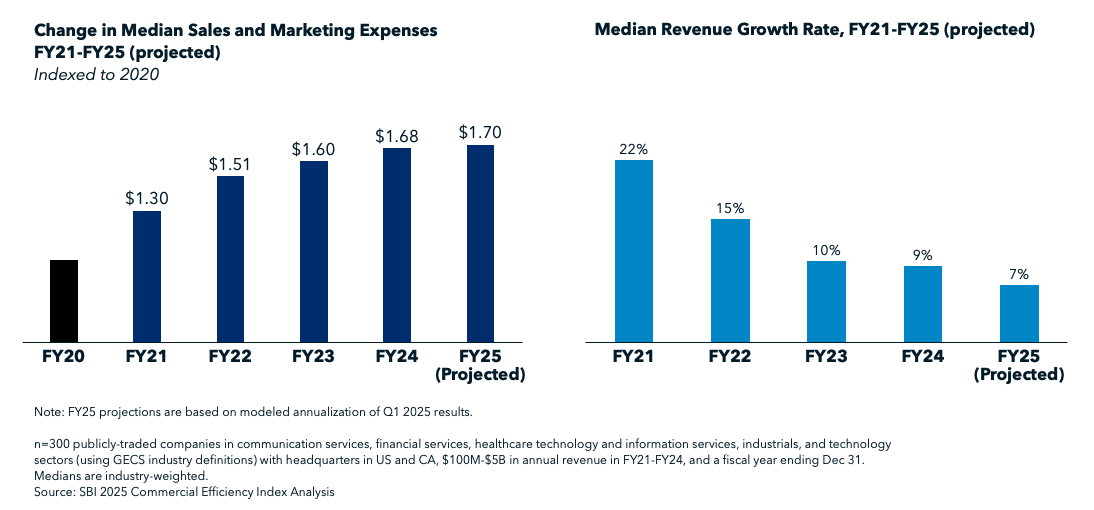

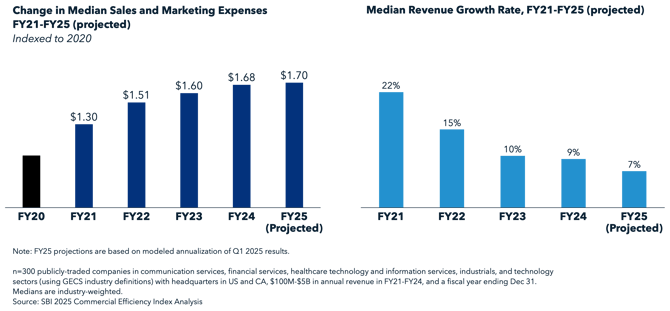

Commercial efficiency continues to be a problem for most companies. While the rate of acceleration is slowing, sales and marketing expenses have grown by 68% since 2020 (including an additional 8% in 2024). But revenue growth rates have declined from 20% to 9% over that same period. The yield on sales and marketing spend is low for most organizations across most sectors.

These double-negative trends cannot continue much longer. While costs are coming under control, we know that sales and marketing spend in general correlates to growth. The key is allocating that spend in the right way, which requires more than a bold bet, a gut instinct, or a simple trending of past year performance. A robust planning process that provides ample time to investigate the right areas for commercial spend is critical for ensuring that spend drives high-quality growth.

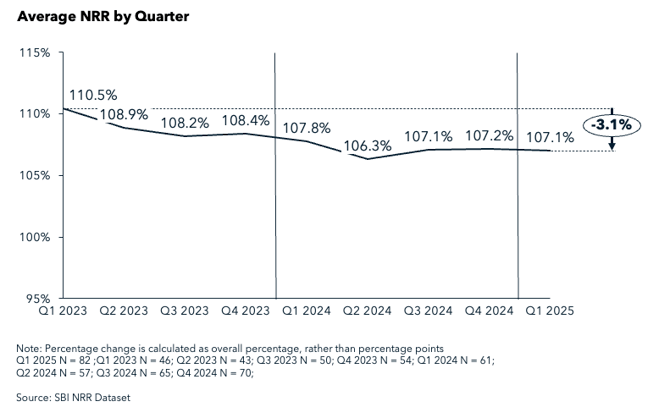

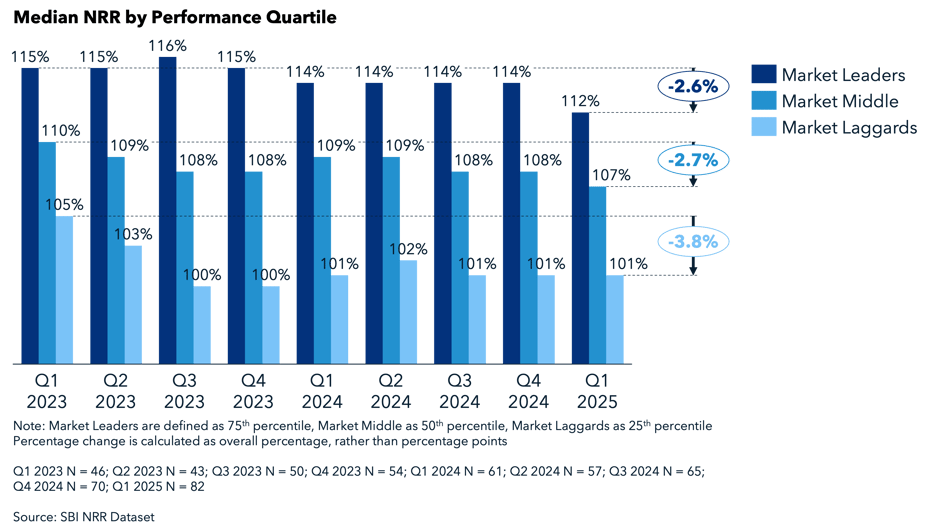

NRR is Steadily Declining

Average net revenue retention (NRR) dropped 3.1% (3.4 percentage points) over the past two years - from 110.5% to 107.1%. This is notably below healthy expansion levels.

Our research finds that this trend has been fairly widespread. Looking across “tiers” of NRR, declines have been just as steady for higher-performing companies as they have been for lower-performing companies. This is especially concerning given the heavy emphasis companies are placing on expanding the base to combat a challenging growth environment. Our surveying has consistently found that companies expect more than 60% of their net new revenue to come from their existing base of customers.

The NRR trends we are seeing, however, suggest that company economics, and reliable sources of growth, may be shifting right in front of us. It’s critical to understand early whether NRR trends are driven by service issues, challenges with the offering, or shifts in the way customers think about the product and its value. This investigation must begin urgently so that leadership teams can make the right decisions on resource allocation, commercial talent, and account prioritization to ensure strong performance in 2026.

AI is Simultaneously Transforming the Product and Execution

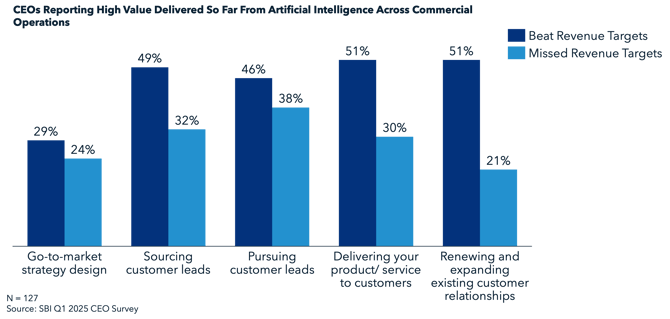

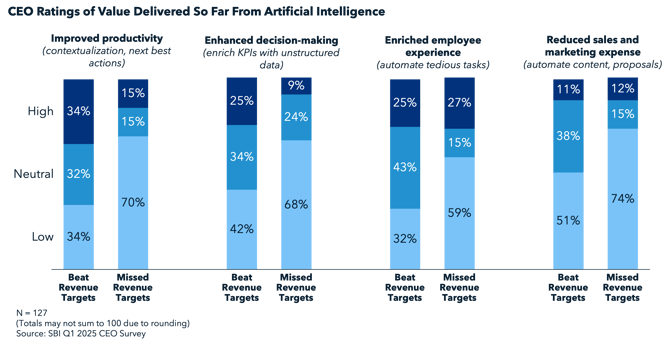

Most companies — software companies in particular — have incorporated artificial intelligence into their offerings. Far fewer have been able to put AI to work at scale for better commercial execution. This failure to launch AI systematically for execution comes as an increasing number of CEOs anticipate commercial headcount reductions due to AI. We do see, however, evidence that those companies that are getting more value out of artificial intelligence in their commercial execution are also reaping the benefits in commercial outcomes.

Leading companies are demonstrating a direct relationship between AI-driven value and better revenue realization. And importantly, they are getting that value differently. We see them in particular to be more than twice as likely to be getting high value from AI for driving productivity, and nearly three times more likely to be getting high value from AI for decision support. In short, they are using AI to drive strategic value and differentiation, not simply cost savings or automation of tedious tasks.

AI as a core part of the product, and for improving execution, will only continue to accelerate for years to come. This has real implications for planning. There are new offerings to introduce, expand, price, and potentially renew for the first time, increasing the risk of faulty models. This gets coupled with tools that carry high promise for improving efficiency and dramatically shifting capacity models. Planning models require more varied and newer inputs than usual, making accuracy more challenging. At the same time, the risk of getting things wrong is higher than ever, as companies can find themselves over-resourced and inefficiently executing.

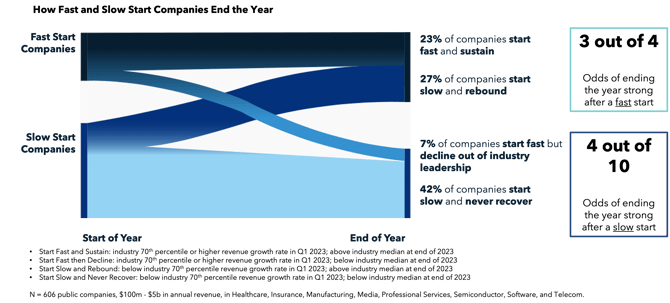

A Fast Start is Critical To Full-Year Success

While it has always been known that a fast start to the year matters, most leaders have treated the concept casually, as opposed to a critical business driver. But our research finds that companies that beat their industry peers in Q1 see a 6x higher full-year revenue growth rate than those same peers. And those that get off to a slow start have no better than a 4 in 10 chance of reversing course and ending the year as an industry leader. A fast start is not nice-to-have, it’s an imperative.

A fast start is only possible when the commercial engine is ready to go on day one, if not before. Companies that start their planning process too late either end up truly starting their year too late, or starting it with a plan they know is not as strong as it needs to be.

This Year Planning Will Be More Uncertain, More Different, and Higher Stakes Than Ever

Some of the factors influencing planning shared here — like the importance of a fast start, or declining NRR — are variations on themes leaders have been grappling with for a number of years. Others — like artificial intelligence, or even commercial efficiency — are new factors that leaders are perhaps contending with for the first time. Together the five make it clear that an early start, deep business intelligence, and best practice planning approaches, are critical to ensure a high-confidence plan.

We advise that leadership teams get started in earnest identifying their big bets for 2026. Where will your growth and efficiency come from? What are the strategic levers you will pull? What will their impact be, how long will they take, and where do you have execution gaps that will make them hard to pull off? This should be more than a brainstorming exercise — come with a strong fact base that you can query as-needed and use to model out scenarios and impacts.

With these big bets in hand, establish your set-back schedule from SKO (which should be as early in the year as possible; even better in December) for building out the foundations of your go-to-market engine — your ICP definitions and account targeting, coverage plans, territories, organizational changes, and comp and quota plans. You can conduct these activities in a vacuum and continue to be impacted by trends like what we described here. Or you can do them in context, with a blank sheet and rigor, to ensure your commercial engine is resilient regardless of the broader market.

We dive deeper into each of these five trends, including questions to ask and steps to get started now, in this report.